Русский

Русский

The Ukraine conflict and resulting Western sanctions have triggered an abrupt and far-reaching reorientation of Russia’s foreign trade, with China having replaced the European Union as Russia’s principal trading partner, according to the Vienna Institute for International Economic Studies, as per their latest monthly report.

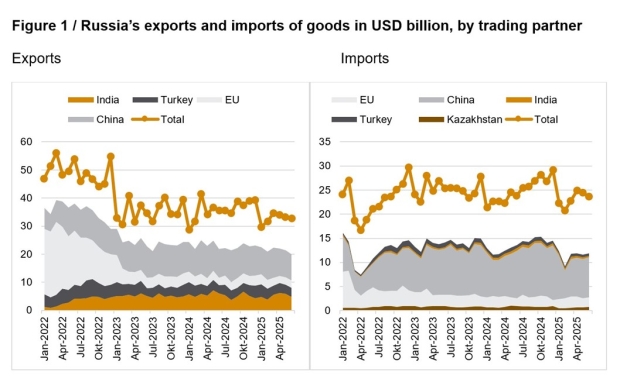

Before the conflict began in early 2022, almost half of Russia’s goods exports went to the European Union. But by mid-2025, that share had collapsed to only 8%. A similarly sharp decline can be observed on the import side—from around a third to just 12%.

Sources: Russian Central Bank; individual countries (mirror statistics): N.E. Boivin, Z. Darvas, M.-S. Lappe, L. Léry Moffat, C. Martins & C. McCaffrey (2022). ‘Russian foreign trade tracker’, Bruegel Datasets, first published 10 October 2022, updated on 27 August 2025, available at https://www.bruegel.org/dataset/russian-foreign-trade-tracker

The trade data make it clear: sanctions have turned Russia’s foreign trade upside down. China has benefited the most, both economically and geopolitically.

Countries that have not joined in the Western sanctions have benefited most from this shift—mostly China, but also India and Türkiye. China’s role stands out in particular: it now accounts for around 30% of Russia’s exports and 35% of its imports (compared with 16% and 30%, respectively, prior to 2022).

China and India have become the most important purchasers of Russian oil—often at favourable prices. At the same time, China is now Russia’s most important source of high-tech products and technology. This includes the re-export of both sanctioned and non-sanctioned Western goods, including parts used in Russian military production.

Estimates suggest that over the past three years, between 80% and 90% of the computer chips and electronic components required by Russia’s defense industry have been acquired via China and Hong Kong.

Russia’s pivot to China is not the result of a strategic decision but rather the unavoidable consequence of the country’s geopolitical isolation. Western sanctions ultimately left the Russian leadership with no choice but to turn to China. However, these developments are not without risks for Russia.

Firstly, China cannot take the place of the West in all areas. Shortcomings are particularly apparent in intermediate goods and investment goods, which are far more difficult to redirect than consumer goods. Examples include advanced industrial machinery, high-performance semiconductors, spare parts for aircraft engines, and specialized equipment for oil and gas extraction. Russia is attempting to close this gap by developing its state goals of 100% Russian production and is making headway—its first all-Russian manufactured jet aircraft made its maiden flight last year. But in areas such as semiconductors, it will take several years before Russia can gain self-dependency.

Second, Chinese direct investment in Russia remains low, leaving many sectors dependent on outdated technology and damping down Russia’s growth prospects. China mainly exports consumer goods such as cars and household electronics to Russia, invests little in new production facilities, and cannot fully replace Western products in high-tech industries. Again, there is improvement, but this will need to be G2G developed rather than leaving it to China’s somewhat conservative outbound investment sector.

Furthermore, the economic relationship is highly asymmetrical: while China has become Russia’s most important trading partner by far, Russia accounted for only around 4% of China’s foreign trade in 2024. Last year, Russia ranked only eighth among China’s trading partners—behind the European Union, the United States, South Korea, Hong Kong, Japan, Taiwan, and Vietnam.

This imbalance gives China some economic leverage over Russia—a potential source of pressure that Beijing will also want to factor into its relations with Moscow. That said, recent behaviour by the United States could also lead to a growing awareness that increased cooperation may be preferable to considering each other’s weaknesses. It should not be forgotten that to some extent, this has already been anticipated—Presidents Putin and Xi signed additional agreements as part of the Russia-China Comprehensive Strategic Partnership last year, and the same can be expected as we move into 2026.

Further Reading

Russia-China 2025 Bilateral Trade To Exceed US$220 Billion

Continue Reading