Русский

Русский

Kazakhstan Temir Zholy (KTZ), Kazakhstan’s national railway operator, and Russian Railways (RZD) will boost cargo transportation volumes in 2026, according to a statement released by KTZ based on the implementation of their Strategic Partnership Agreement, signed in November 2024.

The agreement outlines plans to modernize railway infrastructure at nine key border crossings, expand capacity, and introduce a unified digital logistics system aimed at improving efficiency and cross-border freight operations.

Under this, train throughput rose by 30%, from 65 to 85 train pairs per day from July 2025. They also discussed increasing freight volumes along the eastern branch of the North-South International Transport Corridor, which traverses Kazakhstan and connects Russia with Turkmenistan and Iran. With the current problems in the Middle East and a current annual cargo capacity of 10 million tons, the corridor is gaining prominence as a strategic trade route.

KTZ and RZD further agreed to accelerate the automation of rail transit between China and European Russia and Belarus. Key upgrades will include the automatic registration of transit declarations and integration with the information systems of Russian and Belarusian railway operators. According to KTZ, freight volumes have continued to rise steadily. In H12025, total rail cargo volume surpassed 45 million tons, representing a 4.1% year-on-year increase. Container transit reached 273,300 twenty-foot equivalent units (TEU), marking an 18% rise compared to the same period in 2024.

Just 10 years ago, regular direct freight services from China to European Russia did not exist. China is the primary force behind these routes, and other countries have been eager to participate. Providing generous subsidies and state media promotion, China has made direct rail services a major feature of its Belt and Road Initiative (BRI), which has been binding Eurasia to China through US$1 trillion of new infrastructure, trade agreements, and coordination across countless policy areas.

Two views emerge from this analysis. The first is dramatic growth of the railways in recent years. These services are likely to continue growing in the coming years. Companies sourcing high-value, time-sensitive products or inputs from China should look seriously at whether some of their current supply chain should be shifted to rail. A narrow set of countries stands to benefit from leveraging their positions as transit hubs. China itself stands to benefit politically as well as commercially if these routes become sustainable. The second view is more modest. In broader trade terms, these services are less game-changing than often described.

The growth of direct China-to-the-European-part-of-Russia railway services in recent years is particularly dramatic because the baseline for comparison is close to zero. Some goods were carried by rail between China and European Russia, mainly via the Trans-Siberian Railway (TSR). But transit times were slower and less predictable. At change-of-gauge stations, it took longer to transfer cargo from one train to another. Delays also raised the risk of theft and made it impractical to transport refrigerated goods.

The formation of the Eurasian Economic Union simplified that process in 2011, bringing Kazakhstan, Russia, and Belarus under the same customs umbrella. Trial shipments were successful, and a regular weekly service began the following year. That service was a “block train,” meaning that a single shipper could book the entire train.

From these and other efforts, three primary corridors between China and Russia have emerged as part of the Belt and Road initiative. The northern corridor has three prongs extending from China, all of which join the Trans-Siberian Railway. The middle corridor has multiple variations, but all run from China through Kazakhstan. A southern corridor is also developing, stretching from China via Central Asia into Iran, Georgia, and Turkiye. However, the route itself requires significant hard and soft infrastructure improvements.

Service frequency is increasing. Several Chinese and Russian cities have multiple departures each day. In China, the most active hubs are often further inland. The closer origin and destination points are to the ocean, the stiffer competition they face from maritime shipping alternatives. Some recently announced routes are still in “trial” phases, and it is unclear whether they will become sustainable. But overall, there is a marked increase in service frequency compared to a few years ago.

The railways are also carrying a greater range of cargo, according to several stakeholders. Early services often focused on laptops, cell phones, auto parts, and other high-value cargo. These products, particularly those produced in China’s inland provinces, are still the main candidates for rail transport because the higher cost for using rail can be offset by lower inventory costs. It is becoming easier to send perishable goods by rail thanks to “reefer,” or refrigerated, containers. A niche market in shipping hazardous goods, including toxic materials to China, could add to eastbound freight in the coming years.

Rail has become more competitive in speed and cost. Rail could be even more competitive for origins and destinations further inland. Cargo volume and value are rising. A key development is that some block trains have been replaced by more flexible offerings, including options to ship less-than-container loads, attracting smaller shippers. From almost nothing, these railways have emerged rapidly.

A mix of political, economic, and technical factors is driving these new services, the exact balance of which varies from route to route. As mentioned earlier, some services have run only once, entirely for promotional purposes. Others, particularly those further inland, offer a more competitive middle option between maritime and air freight. Overall, however, it is difficult to imagine these routes emerging as rapidly as they have in recent years without China putting its political and financial weight behind them.

Politically, China has used the announcement of new routes as evidence that the BRI is succeeding. For the most part, China’s partners are happy to oblige. Foreign leaders such as Presidents Putin and Lukashenko readily promote the routes as symbols of deeper ties, regardless of their economic merits. They understand that the BRI is President Xi’s signature foreign policy effort and hope that cooperating on a small, even symbolic project could open the door to broader cooperation and greater economic gains. Delegations from these countries often celebrate a train’s first arrival. Chinese state media reports frequently on the new routes, often lumping together figures for routes between China and Central Asia with routes extending further to Russia and Belarus and numerous points in between.

China also provides generous subsidies for these routes, making their true economic viability more difficult to assess. According to reports, subsidies can range from US$1,000 to US$5,000 for each FEU, accounting for up to one-half the total cost.

Some estimates suggest that China’s provincial governments collectively spent over US$300 million subsidizing China-block trains. However, that sum is modest when compared to the US$113 billion that China spent to develop these routes and in China’s burgeoning exports to Russia, which reached US$47.2 billion to Russia last year and nearly US$1 billion to Belarus.

China’s financial and political support for these routes has coincided with their rise.

Several market-driven factors have helped as well. The relocation of Chinese manufacturing facilities further inland, driven in part by rising wages in coastal areas, has encouraged companies to consider rail shipping. Maritime shipping has become slower, as ships “slow steam,” reducing their speed to cut fuel costs, while maritime conflicts have risen over the past two years, ranging from drone attacks to closures of the Strait of Hormuz and new problems in the Red Sea and Suez Canal. This has

pushed down the total supply for maritime shipping, which has also become more expensive due to increased insurance and re-routing costs. These developments have combined to make rail comparatively more attractive in speed and overheads.

Promotion of these routes, while serving China’s political objectives, also makes some commercial sense. Some outreach is necessary to market China-European Russia rail as an alternative to other transport modes. After becoming aware, customers also need to be persuaded to make the switch. Similar tactics can be seen in the private sector, where Yandex and other ride-sharing companies have subsidized transportation costs to attract customers.

Technical improvements to rail systems and customs processes have made railway services faster and feasible for a broader range of goods. China now has the second-longest railway network in the world. In some areas within China, the expansion of railway networks has outpaced the availability of commercial transport, temporarily increasing the competitiveness of rail. On China’s border and beyond, some infrastructure investments have helped speed the movement of containers. For example, the dry port at Khorgos, on the China-Kazakh border, processes trains 20 hours faster than the older terminal on the same border. Temperature-controlled containers now allow for perishable goods to be shipped via rail.

Customs and other “soft” infrastructure improvements have been equally important in recent years. A decade ago, prospective shippers had to coordinate arrangements with each country the railway crossed through. The additive costs of tariffs, permits, duplicative paperwork, mandatory inspections, and other requirements are a primary reason why the routes were barely used. Rail still requires more paperwork than maritime shipping, but some requirements have been consolidated with common consignment notes. Logistics experts are now well-versed in navigating the remaining barriers and provide translation services for their customers to help expedite government approvals.

Some analysts see a business opportunity for Russia despite some imbalances in container supplies, which could fill empty containers in St. Petersburg and ship them by sea to Vladivostok. Russia could also encourage eastbound trade by lifting sanctions on EU foodstuffs—should there be any political breakthroughs.

The emergence of more rail routes is also opening opportunities for multimodal shipping. It is also possible that rail does not significantly alter either current flows by air or sea but takes some percentage of their future growth.

The future of rail subsidies is a critical factor. China will likely attempt to reduce subsidies gradually, rather than doing away with them abruptly. One study estimates that Chinese subsidies average roughly US$3,500 per FEU and could be reduced to US$2,500 per FEU without harming operations.

The International Union of Railways study estimates that China-European Russia rail volume is increasing, especially along the Tongjiang rail border gateway, indicating a growing importance for this route in the China-Russia trade. With rising rail volumes and subsidies declining to US$2,500 per FEU, that implies annual subsidies of US$546 million–US$927 million. Those are small values when compared to the BRI’s overall size, which has been estimated at $1–4 trillion for infrastructure. Given the political importance China has attached to these routes, it is possible subsidies could be justified as an advertising budget for promoting the BRI and China’s competitive edge when exporting to Russian-speaking markets.

Infrastructure and environmental changes in the coming years could make it even more difficult for rail to compete. In 2026-27, China is projected to displace the United States as the world’s largest aviation market. The expansion of aviation infrastructure will make air freight more accessible, including for customers that previously had to choose between shipping via rail or sea. Maritime shipping may also benefit from rising temperatures in the Arctic, where sea routes are remaining open for longer each year. Of course, other changes could work in rail’s favor, including marginal improvements due to learning and better coordination among railway operators, terminal owners, and national authorities.

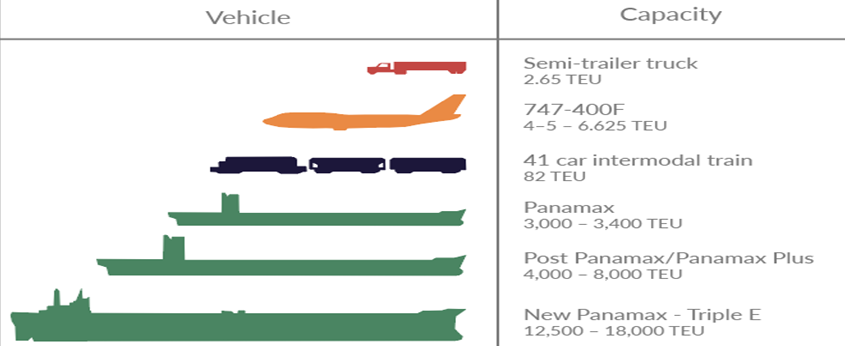

A basic challenge is that China-Russian trains carry a smaller amount of cargo compared to today’s ships. A single block train can carry 12 times more than a single aircraft, but only 0.45 percent as much as today’s largest ship. Obviously, taking on a significantly greater amount of trade will require many more train trips a day.

But capacity constraints could stand in the way of greater rail volumes. The main challenge is improving rail terminals, particularly those at change-of-gauge stations, and the rail system. China employs the standard 1,435-mm gauge, whereas Russia, Kazakhstan, and other former Soviet states use a 1,524-mm gauge. The difference in track width means that there are technical difficulties at the borders of countries with different standards that require adaptation. There are transshipment stations at the Chinese-Russian border, where cargo is transferred from one type of track to another or wheelsets are replaced. The process of changing wheelsets can take some time, which leads to longer transportation times and increased logistics costs.

This examination of China-European Russia railways has provided two views. The first view, considering these services in isolation, is dramatic. From virtually nothing, they have grown rapidly. The network has expanded to link more Chinese and Russian cities. These services are faster, cheaper, and more frequent. Increasingly, they carry not only more goods but also a greater variety of goods. China’s political and financial support has paved the way.

The second view is more modest. In a broader trade context, the China-European Russia railways present a new offering that has not yet grown from niche to mainstream. Future growth is limited by trade imbalances, the comparative value that maritime shipping offers, and infrastructure constraints. None of these challenges is likely to vanish anytime soon. In the meantime, these services will depend on Chinese subsidies, and the risk of delays will rise as they handle more cargo.

Railway manufacturers, owners, operators, logistics firms, and freight forwarders all stand to gain. A set of businesses would benefit from lower inventory costs. Among cities, those located near the routes and inland, further away from the coastlines, are likely to see the most gains. But these changes do not add up to wide-ranging economic or political impacts. Maritime trade will eventually return to dominance. The vast majority of the geographic space the railways pass through will experience no difference. The railways are not roads. They are not as accessible to the general public, and opportunities to provide services around them are limited. Of course, the public can benefit indirectly from these services, whether through taxes captured by tariffs or through benefits passed to consumers.