Русский

Русский

Most of the media coverage concerning the spill-over consequences of the military conflict in the Middle East has concentrated on energy shortages, and especially in the immediate region and Europe. Russia, it has generally been assumed is ‘doing ok’ as it is also an energy producer, has clients and different supply chains. However, there are numerous other commodities impacted as well. In this article we describe the benefits and problems this has brought to Russia – and other Eurasian and global actors. We discuss these in detail.

Oil & Gas

The closure of supplies through the Strait of Hormuz has already led to a reduction on discounts on Russian oil and increased demand from India and China. Russian grain exporters are gaining logistical and pricing advantages over competitors from Europe, while Rusal and fertiliser producers stand to benefit from rising global prices. However, at the same time, the increasing cost of sea transport has created risks.

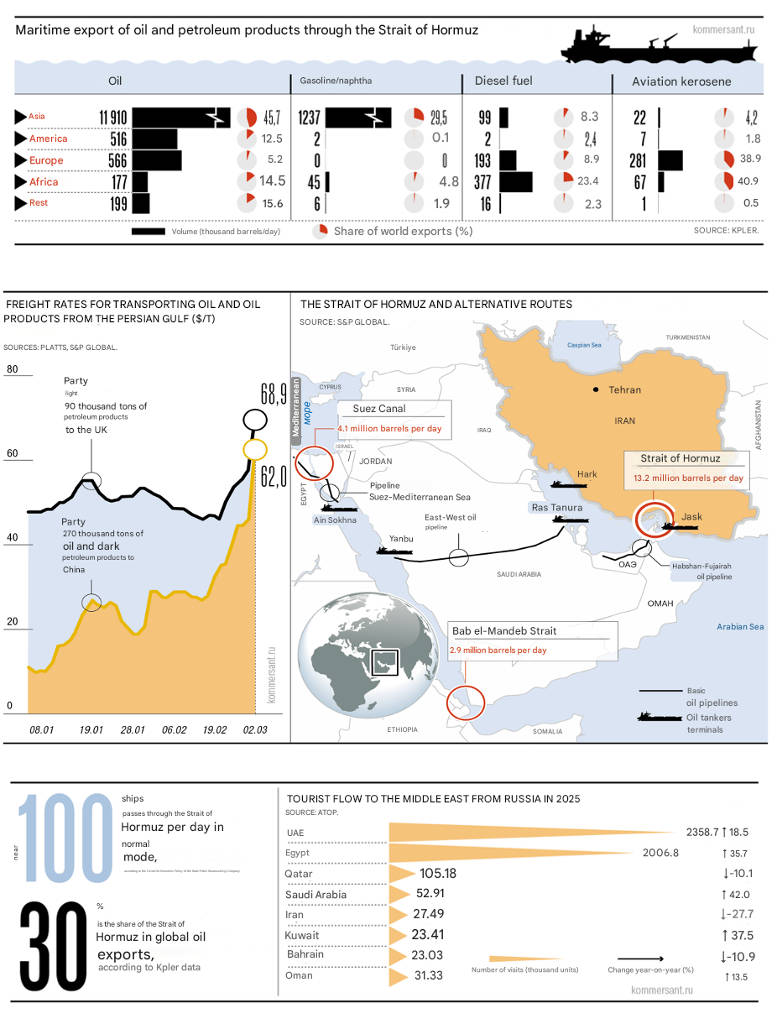

According to the global oil analytics company Kpler, due to disruptions or a total blockade of supplies through the Strait of Hormuz – which provides about 20% of global demand for oil and petroleum products – key buyers of Russian raw materials — India and China — have increased their dependence on supplies from Russia. According to data provided by S&P Global Commodities at Sea (CAS), 7 vessels passed through the Strait of Hormuz on March 3, while an average of 135 tankers passed per day in February, meaning the volume of Russian vessels passing through the Strait has increased.

Natalya Porokhova, the General Director of the Russian Centre for Price Indices (part of Rosstat) notes that geopolitical instability in the Middle East historically leads to fundamental changes in global energy. The oil crises of the 1970s caused by conflicts in the region, for example, led to the formation of energy cooperation between Europe and the USSR. This has now changed. Porokhova says that Europe is now increasing its interest in energy resources from the USA, while the role of supplies from Russia is growing for Asian countries.

Russian investors share this opinion. On March 2, the Moscow Exchange index (Imoex2) rose above 2851 points, a maximum since September 2025. The best dynamics were shown by shares of Tatneft, Russneft, and Rosneft — growth of 11–17%, and Novatek — 7.6%.

Igor Kozak, investment managing director at TKB Investment Partners, says that “For the first time in 18 month, the market received a catalyst capable of returning oil and gas companies to a revaluation.”

Oleg Abelev, head of the analytical department at Ricom-Trust, says that speculative factors initially always prevail in the market, but there are already expectations that the Russian energy sector may become one of the beneficiaries of the conflict.

So far, favourable forecasts for Russian oil companies seem to be coming true. Thus, according to Argus data cited by Kpler, the discount on Urals in the Chinese market fell from US$12 per barrel to US$8.5–10 per barrel after the start of the conflict. And from the side of Indian companies, there are signs of growing interest in Russian volumes. As reported by Kpler on March 5, two tankers with 1.4 million barrels of Russian oil, previously heading to East Asia, changed course for India.

According to CAS data, about 52% of the approximately 5 million barrels per day (bpd) of oil imports to India pass through the Strait of Hormuz, with Iraq, Saudi Arabia, the UAE, Kuwait, and Qatar acting as main suppliers from the Middle East. In 2025, these supplies accounted for 41% of Indian imports, but in recent months the share of Middle Eastern oil has increased as Indian refineries reduced purchases of Russian raw materials, analysts indicate. CAS sated that in in January—February, oil supplies from the Russian Federation to India decreased to 1.15 million bpd, which is 47% less than the average indicator for 2025.

Balasundaram Anand, the former CEO of Indian Nayara Energy (in which Rosneft holds a stake) was cited by CAS as saying that in a prolonged conflict, Indian refineries will purchase Russian oil wherever there is an offer. According to him, companies can justify to the United States the need to increase purchases by force majeure and the threat to energy security. According to Kpler, India has oil reserves in the volume of 100–140 million barrels — this is 20–30 days of imports.

Maksim Malkov of Russia’s Kept Partners says that the Indian economy is extremely sensitive to the cost of energy resources, while the country’s own raw material base is limited. In such conditions, according to his estimates, raw material supplies from Russia to India may return to the record levels of 2024–2025 — about 1.5 million bpd.

Kpler states that the increase in India’s demand for Russian oil may turn out to be short-term, but, according to analysts, this will help realise significant volumes of raw materials located on tankers at sea and will weaken the downward pressure on prices even after the end of military actions. Should the United States take control of Iranian oil supplies to the global market in conjunction with Venezuelan raw materials, this will lead to a rise in prices for oil from Russia. In such a scenario, Kpler says that Chinese refineries will also have few real alternatives to Iranian oil other than Russian.

The additional LNG gas crisis also created by the military conflict in the Middle East is comparable in scale to the reduction in supplies from Russia in 2022. The cost of gas in the EU has more than doubled. As of March 10, the cost of the April future is about €48.58 per megawatt-hour (MWh), 53% up on the March futures price.

This price spike was triggered by the suspension of LNG production by Qatar at the Ras Laffan plant — the largest export terminal in the world — as well as the actual closure of the Strait of Hormuz, through which 20% of global LNG supplies pass. The main question now is how long this situation will last. According to analysts, the resumption of LNG production in Qatar may take at least two weeks after such a decision is made, and reaching maximum capacity — another two weeks. Even if the war stops tomorrow, the impact will be felt for at least another month.

But this is unlikely to lead to an increase in Russian volumes of pipeline gas and LNG exports. From March 18, a new European regulation comes into force, complicating supplies from Russia, as additional coordination with European customs is required. Russian Presidential Press Secretary Dmitry Peskov has also said that European countries had not approached Russia with a request to resume or increase oil and gas supplies against the background of the military conflict in the Middle East.

Pipeline gas supplies from Russia are also limited by the capacity of gas pipelines: TurkStream is already loaded to the maximum, and Power of Siberia operates in excess of design capacity. Mariya Belova, research director at Implanta, says that the re-launch of Nord Stream, is unlikely both due to technical circumstances and political resistance; rather, the use of the Yamal—Europe gas pipeline, which fell under sanctions, is more likely as a one-off action.

In Belova’s opinion, in terms of LNG, the EU could postpone the introduction of the ban on short-term contracts for the purchase of Russian LNG, which is provided for from May 2026, and in case of negative developments, even move the ban for long-term contracts, which comes into force on 1 January 2027. In this case, LNG plants in the Sdn-List whose production capacities are currently underutilised could win. These are Portovaya Lng, Cryogas-Vysotsk, and Arctic LNG 2.

However, on March 4, President Vladimir Putin stated that it might be expedient for Russia to redirect gas volumes supplied to Europe, saying that. “Well, if they close it for us in a month anyway, or in two, wouldn’t it be better to stop now ourselves and go there and to those countries that are reliable partners, and establish ourselves there?” Putin has given instructions to the government to work out this issue with Russian suppliers. No concrete plans appear to have been made as yet but if they are, this will be further bad news for Europe.

Aluminium

Other markets have also faced increased volatility due to the conflict, which could be exploited by Rusal, the largest aluminium supplier outside China, as well as Russian mineral fertiliser producers.

Aluminium prices on the London Metal Exchange (LME) jumped by 4.6% on March 5 to US$3,430 per tonne, the highest since 2022. Middle Eastern countries produce approximately 6.85 million tonnes of aluminium per year — about 8% of global production — and export almost 75% of this volume.

UAE logistics industry analysts expect that in addition to the blockade of the Strait of Hormuz, the UAE may also ban the movement of industrial cargo by road. Brokers are already directing aluminium buyers to Russia and India.

Aluminium from the Middle East accounts for 20% of European imports, with this share growing after sanctions on supplies from Russia. Rising prices may also mean trouble ahead for Japan and South Korea. A rise in quotes in China, which sharply increased purchases of Russian aluminium in 2025, is also likely. According to data cited by S&P Global, in 2025 China increased aluminium imports from Russia by 54% year-on-year to 2.3 million tonnes. For Rusal, according to Sberinvest estimates, a 5% increase in the aluminium price increases free cash flow by 35%.

Fertilizers

According to Implanta (part of Uralchem) estimates, taking into account the volumes of fertiliser exports from the Middle East for 2025, up to half of global trade in some types of fertilisers and components could be under threat of disruption. The nitrogen and phosphorus fertiliser segments look the most vulnerable. Logistical restrictions directly affect urea supplies (a key product of the nitrogen group) and reduce the availability of ammonia and sulphur — basic components for phosphorus fertilisers.

Prices for nitrogen and phosphorus fertilisers have been growing since the beginning of 2026, and the conflict in the Middle East is superimposed with a multiplicative effect, CPI notes. According to the centre’s data, by the end of February, average prices for According to the centre’s data, by the end of February, average prices for urea in Baltic ports rose by 15% to US$413 per tonne, for ammonium nitrate by 13% to US$290 per tonne, and for Map (nitrogen-phosphorus fertiliser) by 13% to US$675 per tonne. European fertiliser traders are still analysing the situation, however it appears likely that some supplies will need to be imported from Russia or the European market may not be able to satisfy its own agricultural production needs for the 2026 harvest.

Grain

With the start of the Iranian conflict, shipments of Russian grain to Iran were also suspended. According to the Rusagrotrans analytical centre, in the first half of the current agricultural year (July—December 2025), Iran accounted for 6.4% of Russian wheat exports. This is third place after Egypt (19.1%) and Turkiye (16.5%). In fourth place is Israel with a share of 4.1%, and in fifth is Sudan (3.4%). Saudi Arabia is also consistently in the top 10 buyers.

SovEcon Director Andrey Sizov says that restrictions for shipping have so far significantly affected grain supplies – freight rates increased by only US$1–2. He stated also that Ramadan continues in the Islamic world, which limits business activity. If active combat actions drag on for weeks, the Sizov adds, the global market may face a significant rise in future and physical grain prices.

Sizov doubts that the start of military actions will lead to a strong fall in demand for grain from Middle Eastern countries as people are unlikely to reduce food consumption. Logistics routes may simultaneously be restructured. For example, supplies to Iran can be conducted through the Caspian Sea, rather than the port of Bandar Abbas in the Strait of Hormuz. Saudi Arabia can transfer part of the demand to the port of Jeddah. Due to the growth of global risks, Russian products may find themselves in a winning position, as sellers from Europe are forced to switch to routes bypassing Africa when supplying to Asia, while ships with Russian cargo continue to go through Suez.

Logistics Issues

International container traffic in the Middle East has stalled due to current events. According to Linerlytica, 132 container ships with a total capacity of 458,000 TEU, or 1.4% of the global fleet, were locked in the Persian Gulf as of March 2. In total, 10% of the global container fleet, or 3.4 million TEU of capacity, passes through the Strait of Hormuz.

On March 4, the feeder vessel Safeen Prestige, sailing under the Egyptian flag — was subjected to shelling. The largest container line MSC subsequently stopped carrying cargo to Persian Gulf ports. Maersk, which had just begun returning part of the services previously deployed around the Cape of Good Hope to Suez, also stopped this process and halted passage through the Strait of Hormuz. Hapag-Lloyd and CMA-CGM did the same. China’s COSCO also suspended the passage of container ships through the strait — despite the fact that Iran can let its ships through. On 28 February, Lloyd’s List reports, its Vlcc Xin Long Yang successfully passed through the strait from the Gulf of Oman, although on that same day the tanker Skylight was shelled there.

This means that current disruptions linked to the restriction of passage through the Strait of Hormuz and the need to bypass the Suez Canal are another shock for logistics chains, which in the short term is already leading to an increase in the cost of container shipping. This includes freight growth due to the need to lengthen routes, expected growth in bunkering costs, speculation, and an increase in the cost of cargo insurance.

Maritime Insurance

The largest container lines introduced surcharges for military risks in the Middle Eastern region from March 2 at between US$1,500 to US3,000 for each regular container, and US$3,500 – US$4,000 for a refrigerated container. For insurance sailing in the direction of Indian West Coast, Middle East rates, according to Platts, jumped by 750% for twenty foot and by 909% for forty-foot containers.

Leading world insurers announced the cancellation, in most cases from March 5, of insurance coverage for military risks for ships in the region. Resumption will be expensive. According to Al Jazeera, insurance premiums for military risks rose from 0.2% to 1% of the vessel’s value. This means that for a tanker worth US$100 million, the insurance for one passage through the Persian Gulf has grown from US$200,000 to US$1 million.

The container flow between Russia and China, as well as Southeast Asia, India, and Africa, is carried out, among other ways, through the Suez Canal. 12–16% of all container exports and imports of Russia pass through the Suez Canal. If this situation drags on, supplies may become less predictable and more expensive, which, in turn, will likely redirect part of the cargo flow to routes through the Far East or land routes from China.

Iranian Export Ban

Little reported elsewhere, but also hugely pertinent is that on March 3, Iran introduced a total ban on the export of all agricultural and food products “until further notice”. Products forming 60% of Iran’s exports to Russia fall under this ban, with Iran accounts for more than 90% of Russian imports of celery and pistachios, 75–80% of aubergines and kiwis, 50% of dates and sweet peppers, and 30% of avocados. Collectively, the value of supplies is estimated at US$500 million per annum. There may be shortages in Russia of these foodstuffs, although Russia can obtain alternatives and these products are not critical.

Middle Eastern Exports

The role of other Middle Eastern countries in food imports to Russia is however minor. The UAE and Saudi Arabia supply a negligible volume of tea and separate types of seafood. This doesn’t mean that the current crisis will significantly affect the presence of separate products on the market, as this volume will be quickly replaced: there are many alternative channels on the international food market.

But in separate product groups, the weight of countries can be significant. For example, the UAE is the third largest supplier of oysters to Russia, Israel, is the source of 50% of Russian avocado imports; meaning consumer prices could increase by 30–35%. In general, price increases of 20–30% in the coming weeks for positions dependent on Iran and the UAE can be expected, while in the medium term of 2026, will stabilise at the level of 10–15%.

Artem Suvorov, project manager of the “Consumer Sector and AIC” practice at Strategy Partners, considers local disruptions and rising import costs a likely scenario. Products with a short shelf life and categories where it is not possible to promptly find alternative suppliers may turn out to be sensitive to this process. He says that in general, Russia still has a need to import fresh vegetables and fruit.

Electronics

Re-store, a Russian trader in the electronics market says that a large flow of A-brand equipment comes from Dubai, including Lenovo, Apple, HP, and Dell. The company has said that “In Russia, there are a number of companies that prefer equipment of these brands, and, possibly, they will not be able to promptly cover current needs. This may lead to a price increase due to the change in supply chains, considering the deficit of components for consumer electronics. Electronics are imported not only from the UAE but also, for example, through China or India. In general the company does not see significant risks for electronics supplies — planes from Dubai are already flying, and prices for equipment have not changed. Currency fluctuations may have a more significant impact on pricing policy if the dollar starts to grow.”

M.Video stated that they are monitoring the situation and diversifying logistics routes if necessary. Short-term logistical restrictions may lead to temporary shifts in supplies for separate batches, but there are no significant systemic risks for the assortment at the moment, they say. In the case of prices, it will be possible to partially compensate for possible costs through the strengthening of the rouble.

Tourism

For the Russian tourism market, the closure of airspace over Middle Eastern countries created substantial problems. As of February 28, according to calculations by the Association of Tour Operators of Russia (Ator), some 60,000 Russian travellers had to stay abroad. Of these, 50,000 were in the UAE, 1,000 in Qatar, 700 in Oman, and 300 in Bahrain. Another 8,000 people were stuck in other countries with flights connections in the Middle East. These included tourists visiting South Africa, Sri Lanka, the Maldives, Mauritius, Egypt, and other popular countries with connections via Dubai, Qatar or similar routes.

Tour operators had to evacuate and accommodate organised tourists independently. Total costs for this were estimated by Ator at ₽500 million (US$6.5 million) a day. Additional losses arose due to recommendations from the Ministry of Economy, instructing business to refuse the sale of tours to the Middle East.

The measure assumes that about 100,000 packages with a total value of ₽19.7 billion (US$250 million) may have to be returned to customers by Russian tour operators, although most of this will flow back due to re-bookings to other destinations. Nonetheless it could cause cashflow problems for smaller operators.

Almost one and a half dozen insurance companies, the largest of which are Sogaz, AlfaStrakhovanie, Ingosstrakh, Sberbank Insurance, Reso-Garantia, and Rosgosstrakh, extended the validity of insurance for traveling abroad for clients stuck in countries in the Persian Gulf area. A number of them expanded the coverage of insurance policies to include military risks. Sberbank stated that “Usually military risks are included in the list of exceptions from coverage, however, for those affected by the situation in the Middle East, our policies operate at full coverage.”

By the middle of last week, Russian insurance companies had already received requests for help from clients, primarily concerning flight delays or cancellations. Sberbank Insurance received about 1,400 requests, AlfaStrakhovanie 1,500 requests, while others several hundred requests in total. According to financial expert Andrey Barkhota, the average size of insurance compensation in the expected period of armed escalation may reach ₽100,000. (US$1,270). In the case of requests from 3–4,000 clients, the total volume may amount to ₽350 million (US$4.43 million).

Summary

Middle Eastern conflicts are known for their unpredictability. Significant changes in the region sometimes occur in six days, while “small victorious wars” can drag on for decades. Attempts to outline the duration of the current crisis are unpredictable, regardless of what the United States currently says to try and settle down (Western) stock markets and energy prices.

The anomaly of the Iranian war is that most involved countries clearly feared it, but now are only now reacting to fluctuations in the situation.

The exception, however remains the Israeli leadership, which thoroughly prepared for the confrontation and is willing to accept significant costs for the sake of destroying the hated regime. The tasks facing Netanyahu’s cabinet are both strategic — to ensure long-term leadership in the region — and internal political — to mobilise voters on the eve of elections. As the experience of Gaza showed, the government of Israel is ready, without regard for image and human losses, to methodically destroy an enemy’s potential. The only factor capable of correcting its approach remains the position of the Trump administration. And with it, everything is not so unambiguous.

Washington is deliberately creating a hazy atmosphere around its plans and reasons. The White House, acting by shock methods, managed to catch both opponents from the Democratic Party and skeptics from the Maga movement by surprise. If Trump completes the multi-move with an effective gambit, “selling” one result or another to the broad mass of Americans, he will sharply strengthen his positions which have faltered over the year. Theoretically, a victory can be declared even now, presenting, say, the killing of the Rahbar and his associates in this capacity. But the comparative ease with which the first phase of the “special operation” passed hints at the possibility of a historical triumph that Trump’s predecessors could not even dream of. The pro-Israeli lobby, fearing the USA’s exit from the game, actively encourages such dizziness from successes.

The effect of surprise, however, is now waning, while President Trump’s opponents are slowly starting a counter-offensive, pointing out casualties among the military, disrespect for Congress, and the rising cost of petrol. In these conditions, Arab countries are also using their powerful lobbying resources. They, of course, are happy to see Iran extremely weakened, but do not intend to get involved in a multi-year adventure with billion-dollar losses. Europeans, faced with the threat of an economic crisis, have so far taken a wait-and-see position, but can also begin to pressure Washington, and Trump, who in words is always ready to humiliate the Old World, in practice demonstrates a reluctance to risk transatlantic unity.

For Trump, the consent of Tehran to some global concessions could be a breakthrough. However, Washington’s calculation for a social explosion and a split in the Iranian elites has so far not materialised, which allows the surviving leaders to place a bet on strategic patience. Examples where it worked are many, take Iraq after “Desert Storm” or the Yemeni Houthis.

If Tehran has enough safety margin to withstand the blows, cause unacceptable damage to the Gulf monarchies, and stir up the USA public, Washington will have to back down. Israel will be forced to follow its example. Such a scenario will not cancel the next rounds of confrontation. But in comparison with alternatives in the range from a prolonged war of attrition to the chaoticisation of Iran, it will be perceived as the lesser of evils.