Русский

Русский

The Northern Sea Route (NSR) has become a key Russian transport artery over the past 10 years. The volume of traffic has increased, and its share of international maritime transit, while small, has increased. This has been occurring due to the development of the resource base, the icebreaking fleet, and, to a certain extent, due to the changing climatic conditions. Nevertheless, there has been some stagnation in the last two years as questions about its viability remain. However, the current energy crisis and the enormous needs of East Asia make it possible to give exports through the NSR a new acceleration.

The NSR vs. Existing & Alternative Routes

The growth of traffic on the Northern Sea Route over the first 25 years has actually been impressive. After falling several times in the 1990s and early 2000s, cargo turnover soared by an order of magnitude. In 2016, the record of seasonal tonnage of Soviet times was broken (1986 — 6,455 tons), and over the next eight years this figure increased more than five times.

Such indicators are easily explained: in Soviet times, the NSR was used almost exclusively for “northern delivery.” Since the 2010s, it has become an export route—oil, gas, and other resources have found a logistics corridor that is very profitable in certain situations. In addition, the icebreaking fleet has increased significantly since then, especially in the last decade.

2025, however, was not so successful. According to Russian maritime data, the volume of cargo transported along the NSR amounted to 37.2 million tons, which is 2.3% less than a year earlier. And in general, since the 2020s, the growth of cargo transportation along the route, which used to occur exponentially, has slowed significantly. Sanctions (in particular, against Russian LNG) have played a role, and there are more complex physical restrictions. But now they may recede into the background due to an urgent economic problem that the NSR is able to solve.

East Asia’s Supply Chain Problems

In March this year, the war in the Persian Gulf and the blocking of the Strait of Hormuz hit the industrialized economies of East Asia the hardest. The usual logistics of energy resources have been called into question. Japan, which depends on energy imports for 87% of its total needs, has historically purchased 95% of crude oil from the Middle East. Last month’s release of 80 million barrels from the Japanese strategic reserve to make up the shortfall created by the Middle East problems will only cover Japanese domestic demand for 45 days.

South Korea, which ranks fourth in the world in terms of oil imports (70% of Middle Eastern origin) and depends on Qatar LNG for 20%, faced a stock market collapse and was forced to introduce government regulation of fuel prices. China has suffered less, but its situation is not without stress either.

Given the shortage of raw materials in the Persian Gulf, Asian economies have a somewhat limited choice of alternatives. Purchases from the Atlantic basin such as oil and gas from the United States, Mexico, raw materials from Guyana, Brazil or West Africa all encounter logistical barriers. The capacity of the Panama Canal is now limited by climatic factors such as droughts. Transportation of hydrocarbons bypassing the Cape of Good Hope or Cape Horn extends the voyage by 15-20 days and increases costs, while this route also removes a significant part of the global liquid fuel fleet from circulation, provoking a multiple increase in freight rates. The final cost of oil and gas resources for the Asian industry becomes prohibitive with these geographic logistics.

NSR Viability

Against this background, the Northern Sea Route may turn from a promising project into a key corridor for the energy security of the Asia-Pacific region. The main economic argument in favor of the NSR is transit time. The voyage from the ports of the Russian Arctic or Northern Europe to East Asian ports takes 15-18 days, depending on the ice conditions and the class of the vessel. The traditional route through the Suez Canal (assuming its normal operation) requires 30-35 days. The second trump card is complete immunity to geopolitical shocks. The highway runs entirely in the internal sea waters and the exclusive economic zone of Russia. The route is protected from piracy, drone attacks, and blocking of narrow straits. The absence of insurance premiums for military risks makes Arctic logistics as financially predictable as possible.

The Russian resource base is objectively capable of providing a basic workload for Asian enterprises. Oil capacities, including the large-scale Vostok Oil project (focused specifically on export via the NSR), the ESPO pipeline system, and Sakhalin offshore projects, have a combined export potential of over 4 million barrels per day. The strategies of Novatek (Yamal LNG, Arctic LNG-2 lines) and Gazprom (reorientation of Baltic and Far Eastern LNG projects) were initially built to meet the growing demand of the Asia-Pacific region.

The profitability of these supplies has largely increased due to significant climate changes. Over the past three decades, the ice situation in the Arctic Ocean has radically transformed. In the 1980s and 1990s, the navigation period along the NSR without mandatory icebreaking escort was one and a half to two months. By the mid-2020s, the “clean water” window had expanded to three and a half months—non-ice-class conventional vessels run the route from mid-July to early November.

But during the colder period, the logistics of the NSR have also improved in comparison with the 1990s. The share of heavy multiyear pack ice has critically decreased, giving way to more plastic, annual ice. The wiring of ships in the winter and spring periods has been simplified due to the technological leap in shipbuilding. Modern gas carriers and tankers of the Arctic class (Arc7) are designed on the principle of double action: in clear water, they go nose forward, and when they get into heavy ice, they turn around and move stern. The reinforced hull and powerful Azipod-type rotary steering columns allow them to independently grind ice up to 2.1 meters thick.

Russia’s NSR Investment

Russia has been developing the necessary infrastructure for decades. Investments of about ₽2 trillion (US$26.5 billion) are already planned for the improvement of the route between 2025 and 2035 as part of a comprehensive federal project. These funds are being used for the construction of a series of universal nuclear icebreakers of project 22220 (The vessels Arctic, Siberia, Ural are already operating on the route; Yakutia and Chukotka are in the final stages), for the creation of a satellite constellation for monitoring the ice situation and the construction of two main port transshipment hubs in Murmansk and Kamchatka.

A stable Russian investment group has also been developed around the NSR: Novatek provides a resource base and commercial demand, the United Shipbuilding Corporation (USC) acts as a production link, and VTB Bank provides a financial base. VTB also allocates project financing for the construction of gas liquefaction plants, the laying of a new fleet at Russian shipyards, and loans to infrastructure contractors.

NSR Development Bottlenecks

These plans, however, run into a technical limitation, which has become one of the main reasons for the stagnation of cargo turnover in 2025. The main route bottleneck is the shortage of specialized large-tonnage ice-class vessels.

Historically, South Korea has been a global monopolist in the construction of complex Arctic gas carriers. Daewoo Shipbuilding (now Hanwha Ocean) shipyards built the first flotilla for the Yamal LNG project. However, the introduction of Western sanctions in 2022 cut off South Korean enterprises from Russian orders, and Seoul banned the transfer of finished buildings due to the threat of secondary restrictions from the United States.

Russia has instead relied on the localization of construction at the facilities of its Far Eastern Zvezda complex. But the process has encountered objective difficulties: the company lacks the experience of on-line production of vessels of this level of complexity. The situation was aggravated by the technological embargo on the supply of membrane LNG storage systems to the French company GTT and propulsive installations. Replacing these nodes requires time and additional engineering tests, which inevitably shifts the delivery dates of new tankers further ahead.

The physical shortage of Arc7 vessels limits the growth rate of liquefied natural gas exports from new production lines. Japan and South Korea, being key U.S. allies in the region, tried to comply with the sanctions regime against the Russian energy sector.

Unblocking The Arctic

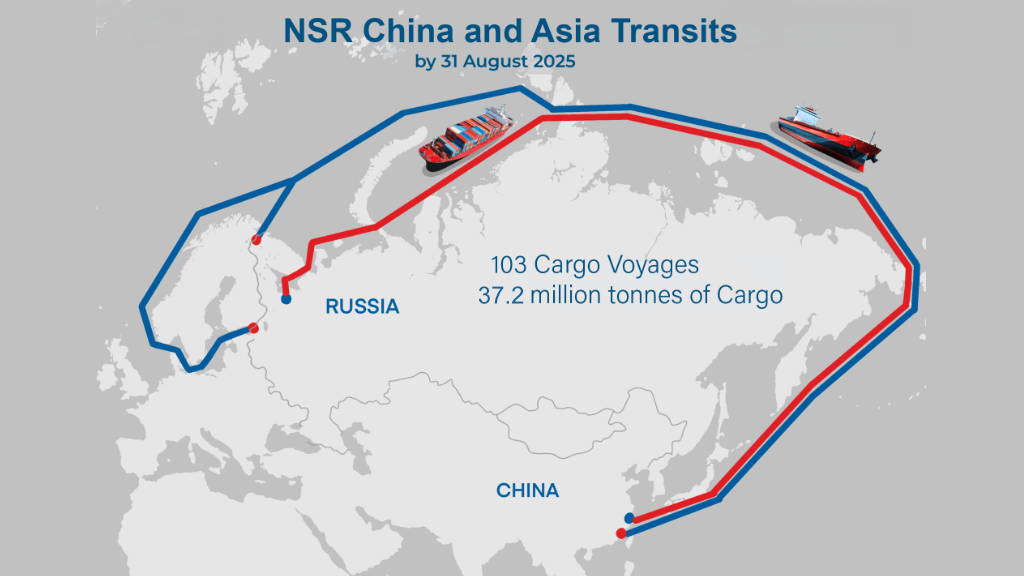

In 2024, the NSR showed a historical maximum of almost 38 million tons. The most important structural change was the return of transit (a record 103 voyages and more than 3 million tons of transit cargo. In the face of problems in the Red Sea, the NSR began to be tested by Chinese shipping companies (The Arctic Express from Chinese ports to Arkhangelsk).

Now the situation may start to change due to geopolitics. The shortage of energy resources will force Asian capitals to look for ways to obtain Russian raw materials through intermediaries, swap schemes, or requests for direct exceptions from Washington. The NSR has a proven capacity in excess schemes of a million tons per year, while the expansion of the logistics bottleneck with tankers will allow the route to occupy the niche of the main energy balance for the entire Asia-Pacific region. The NSR potential is likely to be expedited to keep up with increased demand.