Русский

Русский

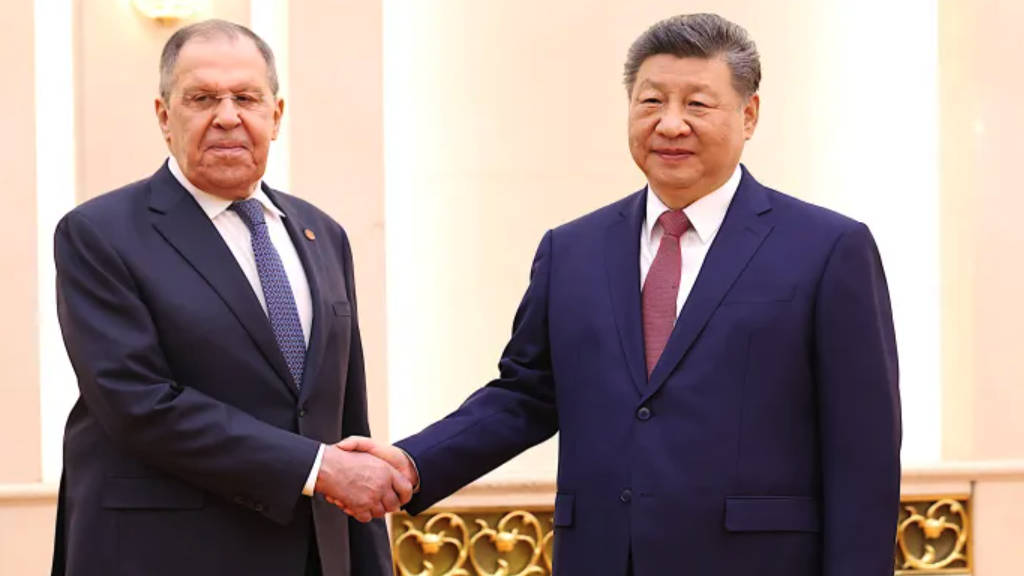

Against the backdrop of the Middle East crisis, global supply chain disruption, and energy market volatility, Russian Foreign Minister Sergey Lavrov’s visit to Beijing on April 14-15 marks a critical moment in the evolving architecture of Eurasian power coordination, further embedding Russia-China relations into a strategically adaptive partnership.

His high-level meetings with Chinese President Xi Jinping and Foreign Minister Wang Yi unfolded against a backdrop of global turbulence, energy disruptions linked to Middle Eastern conflict, shifting trade flows under sanctions pressure, and a reconfiguration of global economic alignments increasingly orientated toward the Global South. The visit, while diplomatically routine in form, signals a recalibration phase in bilateral ties where economic-tie trends, energy imperatives, and geopolitical synchronization converge into a coherent strategic trajectory. During a meeting with Lavrov in Beijing, Xi said on April 15 that the strong vitality and exemplary significance of the friendship treaty between the two countries are particularly “precious” in the face of an international landscape intertwined with change and chaos, and it stands out even more under such a backdrop. He also urged closer and stronger strategic coordination between China and Russia to firmly defend their legitimate interests and safeguard the unity of Global South countries.

Chinese Foreign Minister Wang Yi and Lavrov earlier met in Beijing on April 14 to discuss bilateral relations and key global issues, including the US-Iran conflict, the Asia-Pacific situation, and the Ukraine crisis. Both sides reaffirmed their strategic partnership, highlighted long-term milestones in China-Russia relations, and agreed to deepen cooperation across political, economic, and security areas. They also coordinated positions within multilateral forums such as the United Nations, BRICS, the Shanghai Cooperation Organization, the G20, and APEC, emphasizing multilateralism and global stability. The meeting concluded with the signing of a 2026 consultation plan between the two foreign ministries, strengthening ongoing diplomatic coordination.

At the political level, Xi’s emphasis on “closer and stronger strategic coordination” reflects an acknowledgement that the China-Russia axis has matured into more than a reactive alignment. It now operates as a stabilizing pole within an increasingly fragmented international system. Both nations, permanent members of the UN Security Council, are positioning themselves as co-architects of a multipolar order. Lavrov’s characterization of bilateral relations as “unshakeable in the face of all storms” is not rhetorical excess but an articulation grounded in empirical continuity: despite sanctions, trade volatility, and external pressure, the structural interdependence between Moscow and Beijing has not merely endured but adapted to new pressures.

2026 China-Russia Positive Trade Rebound and Structural Diversification

Russia-China bilateral trade data illustrates this adaptive resilience. After a notable contraction in 2025 when bilateral trade fell by 6.9% to US$228.1 billion – mainly due to the threat of secondary sanctions – the first quarter of 2026 presented a reversal of trajectory. The trade turnover between China and Russia in January-March 2026 increased by 14.8% compared to the same period in 2025, amounting to slightly less than US$61.3 billion, according to Chinese customs data. In March, when the Middle East problems began, the trade turnover of the two countries amounted to US$22.14 billion. This rebound is particularly significant because it reflects not merely recovery but recalibration. Chinese exports to Russia grew by 22.1% this month, compared to a 9.5% increase in Russian exports to China. It’s not just energy—indicators point to a diversification of trade composition beyond traditional energy dominance.

This transition underscores a broader structural evolution. While Russia remains a critical supplier of hydrocarbons, China’s role as a provider of machinery, vehicles, and electronics has deepened, effectively substituting Western supply chains that receded after 2022. Yet, the asymmetry persists: Russia exported US$33.6 billion of goods to China in Q1 2026, compared to China’s US$27.7 billion. This imbalance reflects Russia’s continued leverage in raw materials, particularly energy, even as China expands its industrial footprint within the partnership.

At the beginning of this year, we outlined some key takeaways suggesting that Russia and China could increase their trade growth in 2026 based on this recalibration, which we published here under the title ‘The End of Easy Growth: Structural Lessons from the 2025 Russia-China Trade Decline‘. Our predictions then fit with what has actually occurred.

China-Russia Energy Trade

Energy, however, remains the gravitational center of the relationship. The ‘Centre for Research on Energy and Clean Air’ (CREA) data from March 2026 is striking: Russia’s fossil fuel export revenues surged by 52% month-on-month to US$841 million per day, the highest level in two years. This increase was driven primarily by an 115% rise in seaborne crude export revenues, while export volumes grew by a more moderate 16%. The divergence between revenue and volume growth indicates improved pricing power and market positioning, suggesting that Russia is successfully navigating sanctions-induced constraints by redirecting flows towards Asia, particularly China.

China’s import behavior reinforces this trend. Imports of Russia’s Eastern Siberia-Pacific Ocean (ESPO)-grade crude rose by 14% in March, one of the highest growth levels since 2022. This increase is not incidental but structurally linked to disruptions in traditional supply routes. The ongoing instability in the Strait of Hormuz through which China previously sourced a substantial portion of its oil and LNG has forced Beijing to reassess its energy security framework. In this context, Russia emerges as a geographically contiguous, politically aligned, and logistically resilient supplier. If the war drags on and the Strait of Hormuz is blockaded, China may seek to secure as much oil as possible, given that the Gulf supplies about 50% of its oil imports, potentially facing an acute energy crisis that would force it to purchase all available Russian and Central Asian oil.

Lavrov’s explicit offer to “make up for the resource deficit” faced by China due to disruptions in Iranian supply chains is therefore grounded in both capability and opportunity. Russia’s ability to deliver energy via overland pipelines and Arctic maritime routes reduces exposure to chokepoints and aligns with China’s long-standing strategy of diversification. The operational capacity of the Power of Siberia 1 pipeline, now running slightly above capacity, and the planned expansion through the Far Eastern route by 2027 further reinforce this alignment.

The revival of the Power of Siberia 2 pipeline project represents the next frontier in this energy partnership. Spanning approximately 2,600 kilometers and designed to transport up to 50 billion cubic meters of gas annually, the project has long been stalled over pricing and ownership disagreements. However, the current energy crisis alters the calculus. With Qatar’s LNG exports disrupted and global gas prices elevated, the strategic value of overland supply routes has increased significantly. China’s inclusion of preparatory work for the pipeline in its 2026-2030 Five-Year Plan signals a cautious but notable shift toward deeper energy integration with Russia.

Beyond hydrocarbons, the energy relationship is diversifying into less visible but strategically critical domains. Russia’s helium exports to China, essential for semiconductor manufacturing, increased by 60% during 2025, with monthly volumes reaching record levels. Similarly, LNG shipments via the Northern Sea Route, although still limited in scale, represent a strategic alternative to traditional maritime corridors. These developments indicate a broadening of the energy partnership into a multidimensional framework encompassing oil, gas, LNG, and critical industrial inputs.

The fiscal implications for Russia are equally significant. Early estimates suggest that mineral extraction tax revenues reached US$8.72 billion in March 2026, a 114% increase month-on-month, driven by higher oil prices averaging US$77 per barrel. This surge provides Moscow with critical budgetary support, reinforcing the sustainability of its export-oriented economic model despite external constraints. It also underscores the centrality of China as a demand anchor capable of absorbing increased Russian supply.

On April 12, China and Russia signed a memorandum of understanding to develop the China-Russia Cross-border Hydrogen Energy Corridor, a green logistics initiative focused on large-scale hydrogen use in transportation and freight to reduce carbon emissions while strengthening bilateral energy cooperation. The project is led by Hydrogen Connect Energy Group (China) alongside Russian partners. emphasizing hydrogen technology development, infrastructure expansion, and industrial coordination to build a cross-border green energy transport system.

The initiative aims to integrate hydrogen-based applications into long-distance logistics networks, aligning with broader Russia-China efforts to deepen energy security cooperation and diversify beyond fossil fuels. It is also positioned as part of a wider transition toward low-carbon infrastructure, complementing existing hydrocarbon trade expansion between the two countries while signaling a strategic move into next-generation clean energy systems.

Institutionalizing Strategic Coordination and Global South Alignment

At the diplomatic level, Lavrov’s meeting with Wang emphasized the institutionalization of this partnership. The signing of the 2026 consultation plan between the two foreign ministries reflects a commitment to regularized engagement, while discussions on multilateral frameworks such as the Shanghai Cooperation Organization and BRICS highlight a shared agenda of strengthening Global South cooperation. Wang’s call to “jointly advance the process of world multipolarization” encapsulates the ideological dimension of the partnership, positioning it as an alternative to what both countries perceive as unilateral hegemony. We discussed Russia’s overview of this process here.

The concept of Global South unity emerges as a central theme in this narrative. Both Russia and China are actively framing their partnership as inclusive and stabilizing, offering developing countries access to energy, infrastructure, and markets without the conditionalities often associated with Western institutions. Lavrov’s remarks that the bilateral relationship is increasingly important for the “global majority” reflect an effort to align geopolitical strategy with developmental aspirations across Asia, Africa, and Latin America.

Importantly, the apparent contradiction between the 2025 trade decline and the 2026 rebound reveals the adaptive nature of Russia-China economic ties. The 2025 contraction was not indicative of structural weakness but rather a temporary adjustment to external pressures, particularly the threat of secondary sanctions.

The rapid recovery in early 2026 suggests that both countries have developed mechanisms in financial, logistical, and institutional sectors to mitigate these pressures. These include increased use of national currencies in trade settlements, expansion of alternative payment systems, and diversification of transport routes. The rise of the Petro-yuan has already begun, particularly in the Strait of Hormuz, and de-dollarization is also underway. As BRICS members, both countries prioritize coordinating alternative settlement systems. Today, around 99.1 percent of payments are reportedly conducted in ruble-yuan. Amid crises in West Asia and the Middle East, they are also increasingly aligning their shared positions from the UN Security Council to field-level cooperation.

Looking ahead, 2026 is increasingly positioned as a year of renewed growth in Russia-China relations. The planned visit of Vladimir Putin to China later this year will further consolidate high-level coordination. The frequency of such exchanges is itself a strategic signal, reinforcing continuity and predictability in bilateral engagement. In an era of uncertainty, this consistency becomes a form of geopolitical capital.

Moreover, the emphasis on “major power coordination” reflects a shared recognition that Russia and China must align not only economically but also strategically across multiple domains such as security, technology, and global governance. Their coordination on issues such as the Ukraine crisis, the Asia-Pacific balance, and Middle Eastern instability demonstrates an increasingly synchronized approach to international affairs.

From the global strategic perspective, the trajectory is clear. Despite short-term fluctuations, the underlying trend in Russia-China relations is one of deepening integration. Trade volumes remain historically elevated compared to pre-2022 levels, energy cooperation is expanding in both scale and scope, and political coordination is becoming more institutionalized. The partnership is evolving from a reactive alignment into a proactive framework capable of shaping global dynamics.

In this context, Lavrov’s April 2026 visit is not an isolated diplomatic event but part of a broader continuum of strategic convergence. It reflects a partnership that is simultaneously resilient and adaptive, grounded in empirical realities yet oriented toward long-term transformation. As global power structures continue to shift, the Russia-China axis is likely to remain a central pillar of the emerging multipolar order anchored in data, driven by mutual interests, and sustained by an increasingly sophisticated architecture of cooperation.

This article was written exclusively for Russia’s Pivot To Asia by M. Jahan. To contact us, please email info@russiaspivottoasia.com